Stock in Focus: Alibaba Group Holding Limited (NYSE:BABA)

CommSec

CommSec

22 June 2026

Is Alibaba destined to continue unlocking hidden treasures?

Ali Baba and the Forty Thieves is arguably the most famous of the folk tales found in the One Thousand and One Nights collection. The eponymous hero, a poor but honest woodcutter, discovers the secret treasure of a thieves’ den, which he’s able to enter by saying the magical phrase, “Open sesame!”1

All of which was presumably front of mind in 1999 for businessman and philanthropist Jack Ma when he founded alibaba.com, the e-commerce giant often referred to as “the Amazon of China”.2The company, headquartered in Ma’s home city of Hangzhou, provides consumer-to-consumer (C2C), business-to-consumer (B2C), and business-to-business (B2B) sales services via Chinese and global marketplaces, as well as local consumer, digital media and entertainment, logistics, and cloud computing services. It owns and operates a diverse portfolio of companies around the world in numerous business sectors, and is the world's largest online and mobile commerce company as measured by gross merchandise volume.3

On 19 September 2014, Alibaba's US initial public offering (IPO) on the New York Stock Exchange (NYSE) raised US$25 billion, giving the company a market value of US$231 billion and by far the largest IPO in world history at that time.4 The company is also tradeable on the Singapore and Hong Kong stock exchanges.5

The source of Alibaba's success

Alibaba operates some of China's largest online marketplaces, including Taobao (C2C) and Tmall (B2C). Additional revenue sources include China wholesale e-commerce, international retail and wholesale e-commerce, local consumer services, travel services, cloud computing, digital media and entertainment, Cainiao logistics services, and other businesses.6 It was named the world’s 33rd-largest public company on the Forbes Global 2000 list in 2025.7

“Alibaba is monetizing its network effect better than any other e-commerce platform in China,” says Morningstar.8 “Short-video platforms [such as] Douyin and Kuaishou have not proved they can monetize the physical goods e-commerce market with a durable profit margin." Morningstar also notes Alibaba has historically been profitable and expects continued profitability, subject to competitive pressures.

“We see Alibaba remaining as a key e-commerce marketplace for consumers due to its vast range of stock-keeping units, logistics, infrastructure, operational expertise – [including] governance of products and merchants and protection of consumers – and tools for merchants to manage full product lifecycles. It is the largest e-commerce platform that provides its merchants with predictability in sales and production volume, which leads to predictable production costs.”9

Can't spell "Alibaba" without AI

As with all other global tech giants, Alibaba sees its future prosperity in the brave new world of artificial intelligence (AI). On 24 March 2026, its research arm Damo Academy unveiled a chip designed to fuel AI agents that it claims to be the most powerful of its kind globally.10 According to the company, the chip’s open-source RISC-V nature “allows chip designers to customize instruction sets and accelerate specific AI workloads with no or low licensing fees. This is particularly important for the development of AI agents”.11

Morningstar believes Alibaba’s predicted strong growth “will be driven by artificial intelligence cloud, model-as-a-service offerings, and AI applications.12

“Additional demand is emerging rom the education and healthcare sectors, as well as from companies developing tools that leverage Alibaba’s open-source model for artificial intelligence training,” says Morningstar.13

But what do the bears say?

It’s not all clear skies and smooth sailing ahead for Alibaba, despite its strength in the current global marketplace. Morningstar argues that while it’s “optimistic about Alibaba's ability to become a preferred partner for international retailers and consumer brands looking to sell in China, the firm does not enjoy the same network effect and brand recognition in other countries, and it may face challenges directly expanding in these markets”.14

Additionally, Alibaba’s “expansion into the nonphysical goods marketplace businesses and other regions leads to lower-than-expected margins, and the timing of profitability is delayed”.15

Bears highlight increasing competition in China’s e‑commerce market, with Alibaba losing market share to competitors such as PDD and Douyin and no clear short‑term resolution identified. They also note that investment to maintain competitiveness is expected and may lead to a decline in margins over time. Morningstar highlights regulatory scrutiny in China, including prior enforcement action for anticompetitive practices and ongoing government oversight. Reflecting these factors, Morningstar assigns Alibaba a High uncertainty rating.

Nevertheless, Morningstar offers a fair value estimate of US$258 for Alibaba shares, noticeably higher than the US$132.26 the company landed on at close of trading on 5 May 2026.

Source: CommSec, as of 5/5/26.

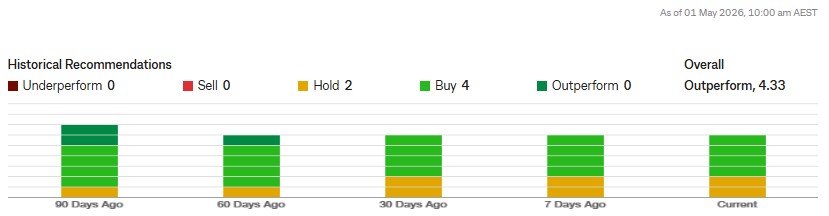

The consensus view

"Consensus: Outperform" in stock trading means the average sentiment among a handful of financial analysts is that a stock will perform slightly better than the overall market or its sector peers over a specific period. Alibaba has maintained an “outperform” consensus since 24 November 202116 – although, as always, past performance is not a reliable indicator of future performance.

Source: CommSec, accessed 5/5/26.

Looking for more exposure opportunities to the Chinese market? Check out this ETF in Focus article on IZZ, an ASX-listed ETF that includes Alibaba, which we've written as part of our “ETF in Focus” series.