![]()

Create knowledge, create wealth

It's never too late to start.

Go from zero to investing hero.

![]()

Create knowledge, create wealth

It's never too late to start.

![]()

There’s something for everyone

Learn the basics of investing or brush up on your skills.

![]()

Learn anytime, anywhere

Enjoy bite-sized learning topics in the palm of your hand.

![]()

Start your investing journey on the right foot

Get up to speed on investing in the sharemarket and beyond.

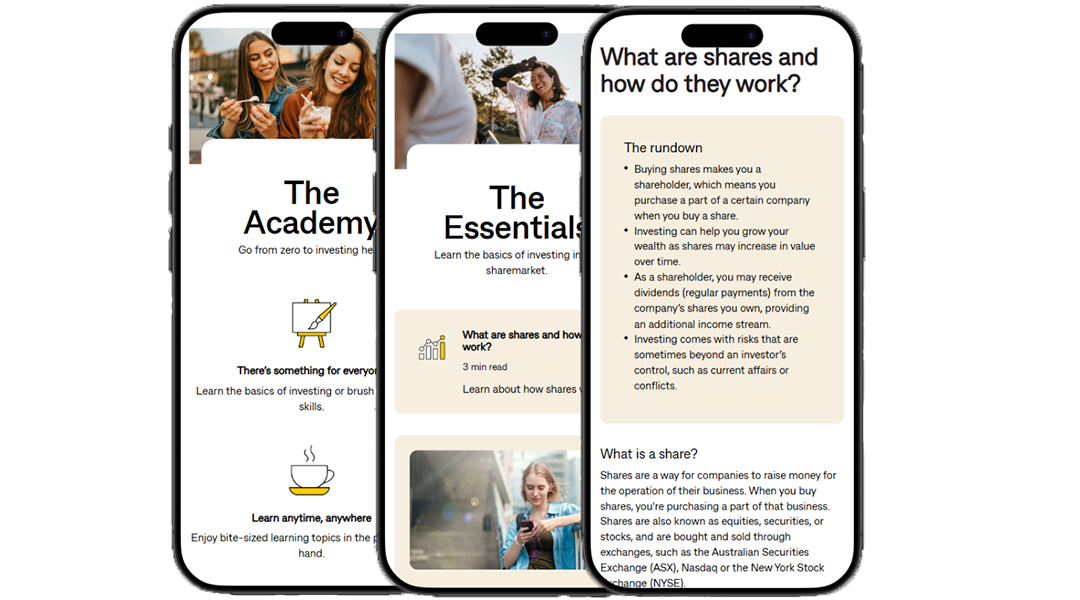

The Essentials

Learn the basics of investing in the sharemarket.

3 min read

Shares are a way for companies to raise money for the operation of their business. When you buy shares, you're purchasing a part of that business. Learn about how shares work.

3 min read

By understanding the costs of investing, you’ll have a better idea of how much money you can make from an investment. Learn about the different costs associated with investing.

6 min read

Every investor’s go-to guide on the most common investing terms.

2 min read

Investing in shares could help you build your wealth more effectively than saving alone. Discover how investing could help you achieve your financial goals.

The Next Level

Already know the basics? Level up your investing knowledge.

4 min read

Diversification is an investment strategy that involves spreading your investments to reduce risk.

2 min read

Invest in the sharemarket with confidence. Discover how you can avoid these common investing mistakes.

1 min read

Blue-chip stocks are shares distributed by well-established, trusted and reputable companies. Learn more about blue-chip stocks and how to spot one.

2 min read

Understand the tax implications of investing in shares in Australia, from the nuances of capital gains tax to franking credits.

Tax Time

Tax time made easier. An investor’s guide to the End of Financial Year (EOFY).

Explore some ways you could prepare for tax time as an investor, including keeping track of your investment records and more.

Learn about how you can access your statements to prepare for tax time.

2 min read

Learn more about what you can claim at tax time.

4 min read

Shares, property or other assets you own could be subject to the capital gains tax (CGT) rules. Learn more about CGT.

Under the spotlight: IPOs

From boardroom to bell ring. Explore the stories and market dynamics behind a company's public debut.

Master the markets

More from The Academy, only available on the CommSec app.

The Game Plan

Plan your next move and start investing with confidence. What you'll learn:

The Mastery

Take control of your portfolio with advanced tools and strategies. What you'll learn:

Bite-sized learning, big-time impact

As a CommSec customer, you'll gain full access to The Academy in the CommSec app, so you can level up your investing knowledge anytime, anywhere.

|

|

Learn on the go

Discover the ins and outs of investing with the CommSec Invest podcast.

Most popular articles

2 min read

Dividends are payments made by a company to its shareholders from its earnings or reserves. They allow investors to share in the company's profits.

3 min read

There are four main types of investments, also known as asset classes, each with their own benefits and risks. Find the investment type that’s right for you.

2 min read

Investing in shares could help you build your wealth more effectively than saving alone. Discover how investing could help you achieve your financial goals.

2 min read

When you invest in shares, the value and price of shares can fluctuate. Sometimes, external factors like conflict or political events can affect the market. Discover how you can manage risks when investing.

Limited time only. Terms and conditions apply.

Help when it matters

All the help you need, all in one place.

1 $5 brokerage for trades up to and including $1000. To be eligible, you must trade online, be CHESS Sponsored with CommSec and settle your trades through either a Commonwealth Direct Investment Account (CDIA) or a CommSec Margin Loan.

The Academy is intended to provide general information of an educational nature only. It is not intended to provide any tax advice.

The Commonwealth Direct Investment Account is issued by Commonwealth Bank of Australia ABN 48 123 123 124 AFSL 234945. This product is administered by Commonwealth Securities Limited ABN 60 067 254 399 AFSL 238814 (CommSec), a wholly owned but non-guaranteed subsidiary of the Commonwealth Bank of Australia.

You can view the Share Trading Terms and Conditions, CommBank Transaction, Savings and Investment Account Terms and Conditions, CommSec Best Execution Statement, Financial Services Guide, Margin Loan Product Disclosure Statement, Margin Loan Terms and Conditions, Exchange Traded Options Product Disclosure Statement and Terms and Conditions and should consider them before making any decision about these products and services.

The Commonwealth Direct Investment Account TMD can be located on the CommBank website. The Exchange Trades Options TMD can be located on the CommSec website. There can be high levels of risk associated with trading in Options; only investors familiar with the risks of Options trading should consider these products.

CommSec Margin Loans are issued by Commonwealth Bank of Australia and administered by Commonwealth Securities Limited.

Warrants are financial instruments issued by banks and other institutions which are traded on ASX Limited and Cboe Australia Pty Limited. They are a form of derivative giving the holder the right to trade (Buy or Sell) or cash settle the underlying instrument (eg shares in a company, a currency, an index or a commodity or a managed investment) with the warrant issuer for a particular price at a particular time according to the terms of issue. Warrants are issued pursuant to a Product Disclosure Statement (PDS) which may be amended or supplemented from time to time. You should carefully consider the PDS before making any investment decision, including whether to acquire, or continue to invest in that product.

Any securities or prices used in the examples given are for illustrative purposes only and should not be considered as a recommendation to buy, sell or hold. Past performance is not indicative of future performance. Investing carries risk

CommSec Mobile App is free to download however your mobile network provider may charge you for accessing data on your phone. CommSec Mobile App Terms of Service can be found at https://www.commsec.com.au/features/commsec-app.html.