CommSec

CommSec

1 July 2026

Author: James Gruber is Equity Market Strategist at CommSec

It has been quite the financial year for the Australian share market. There was a war, an interest rate cut before three rate rises, an AI boom, worries about AI’s impact on sectors and jobs, ongoing tariff uncertainty and plenty of big stock winners and losers.

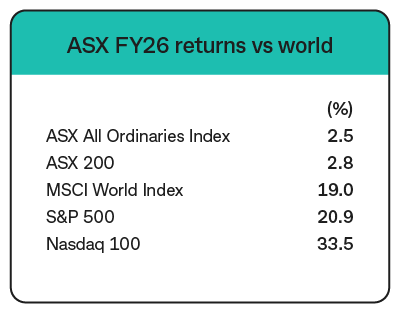

There is a perception that the ASX 200 has performed poorly over the year. However, the index still rose 2.8% in price terms, and 5.9% in total net returns (including dividends). While the latter is well below the historical average index return of close to 10%, it still seems reasonable given the circumstances.

If you look at how Australia has fared versus overseas markets though, the picture is less favourable. The ASX 200’s 2.8% return in price terms in FY2026 trailed the MSCI World Index’s 19.0% return and underperformed the major US indexes by an even wider margin.

Note: Returns are in price terms. MSCI World Index, S&P 500 and Nasdaq 100 are in US dollars while the ASX indexes are in Australian dollars. Source: LSEG

Why has the ASX lagged? Put simply, Australia has had relatively limited exposure to the companies that have driven the global AI rally, as well as company-specific issues which negatively impacted some of the country’s largest blue-chip companies.

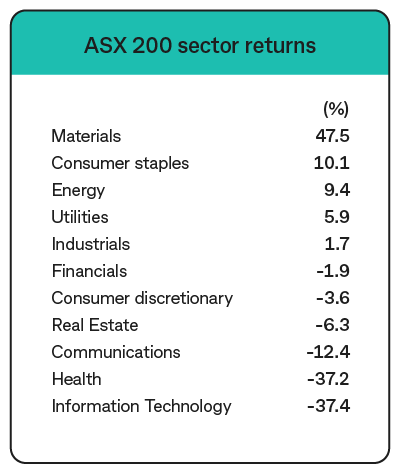

ASX 200 sector performance

Let us break down the ASX 200’s FY2026 performance by sector:

Returns in price terms. Source: IRESS

Materials have held up the index, gaining 48% over the past year.

The sector was led by heavyweights, BHP and Rio Tinto, up 62% and 63% respectively. Both companies were seen as indirect beneficiaries of the AI boom, with growing demand expectations for copper, an essential metal for electricity infrastructure and data centres, supporting sentiment towards the miners.

Consumer staples were the second-best performing sector in FY2026, rising 10%. Woolworths gained 29% as its turnaround strategy gained traction with investors, while supermarket competitor Coles also advanced 17%.

Energy was the next best returning sector, which is not surprising given the impact of the US-Iran war on the global supply of oil and gas, albeit the sector pulled back from peaks following the signing of the interim peace deal.

Financials held up during FY2026, with ANZ recording the strongest share price gains among the Big Four banks, rising 21%.

The worst performing ASX sectors were healthcare and technology, both down 37%.

With healthcare, CSL was among the largest blue-chip decliners, with shares falling 52% following write-downs, management upheaval, and concerns about future earnings.

Cochlear outdid CSL, dropping 59%, as demand issues in the US market led to a series of profit downgrades, one of which in April resulted in the stock falling 40% in a single day – its worst-ever decline.

The information technology sector also dropped heavily through the year, with WiseTech down 70% amid corporate governance concerns and worries about AI’s impact on software and software companies, while Xero fell 60% amid similar sector pressures and concerns about its US business.

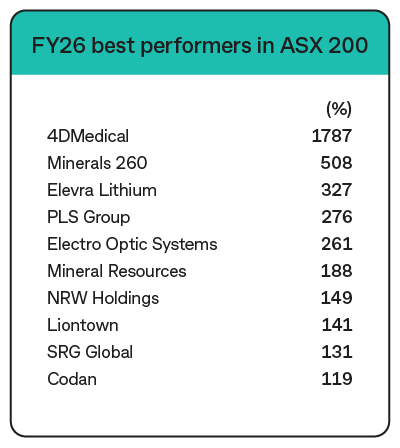

The biggest ASX 200 winners in FY2026

Here is a list of the top 10 performers on the ASX 200 over the past 12 months:

Note: Returns in price terms. Source: IRESS

4DMedical soared as it made significant progress in commercialising its technology in the US. The company's flagship CT:VQ software - which generates ventilation and perfusion images from a standard CT scan - received US FDA clearance and has gained rapid adoption in leading US hospitals.

Electric Optic Systems rose as increased defence spending, both locally and overseas, supported both the company and broader investor sentiment towards defence stocks.

The remainder of the top 10 performers were all mining-related stocks.

Mineral Resources had a big year, following an operational turnaround after several challenging years.

The biggest ASX 200 losers in FY2026

Here is a list of the worst performing stocks in the index:

Note: Returns in price terms. Source: IRESS

We have mentioned the falls in the likes of CSL, Cochlear, WiseTech, and Xero.

SEEK dropped amid weaker hiring conditions, AI-related concerns, and valuation compression.

Meanwhile REA fell on weaker housing conditions and greater competition.

Lendlease continued its fall as a turnaround flagged in 2024 has taken longer than expected, and debt issues continue to concern investors.

The outlook for FY2027

The outlook for the ASX 200 will, in part, be influenced by the miners, with materials accounting for 27% of the index and BHP alone the largest weighting at 11.7%. Will ongoing investment in AI and data centres continue to support demand expectations for commodities such as copper? What impact will the Middle East conflict have on commodity prices?

The other sector heavyweight is the banks, where the outlook will be influenced by interest rate movements and broader economic conditions, with budget measures also a factor.

Markets will be watching whether the healthcare and technology sectors can recover from a difficult year.

With healthcare, will CSL and Cochlear be able to stabilise earnings and rebuild investor confidence after dramatic recent falls? Any turnaround in these stocks may go some way to restoring investor confidence in the healthcare sector.

More broadly, investors will be closely watching the economy and the fate of interest rates. Will interest rate rises in the first half of the calendar year continue to feed through to economic activity and company profits for the next 12 months? Is this the end of the recent rate hiking cycle? Can the economy break its productivity growth drought? Will efforts to tame inflation pay off?

Markets will be eyeing whether an interest rate pause, or eventual cuts, provide support for economic activity, domestic-facing ASX companies and company earnings.