CommSec

CommSec

18 June 2026

Author: James Gruber is Equity Market Strategist at CommSec

One question that investors often ask is how to build a simple portfolio from the ground up - one that is straightforward to create, easy to manage, and suitable for long-term investing.

This article outlines some general principles that investors may consider when building a portfolio.

To begin, there are several core principles of portfolio construction that are backed by decades of academic research:

1. Asset allocation can often have a greater impact than individual stock selection

How a portfolio is divided between asset types (stocks, bonds and cash) can have a significant influence on long-term outcomes.[1]

For example, if you have a portfolio of 80% stocks/20% bonds, then a 30% fall in stock markets will produce a meaningful drop in your portfolio because most of it is in stocks.

However, if your portfolio is 20% stocks/80% bonds, and stock markets tumble 30% while bond markets remain stable, then your portfolio could experience smaller declines.

That is why the mix of assets could matter more than which stocks you pick.

2. Diversification can help manage portfolio risk

A key finding from academic research is that it is possible to reduce risk without giving up expected returns, just by spreading your money around (though the quality of diversification matters more than the number of assets).[2]

In simple terms, if you only invest in one company, and it does well, that can be positive for your portfolio, but if it does not, then you can end up in trouble.

Now imagine that you invest in many different things, some of which go up, and some go down, but the ups and downs balance each other out – the overall result becomes smoother and less risky.

3. Markets are (broadly) efficient

Markets are generally efficient, especially large, liquid ones, because:

- Prices already reflect publicly available information.

- Consistently outperforming the market can be difficult, particularly after fees and taxes.[3]

4. Risk and return are inseparable

In general, investments with higher return potential also tend to involve higher levels of risk.

For example, stocks have historically delivered some of the highest long-term returns compared with other major asset classes, though outcomes can vary depending on the market and timeframe.[4] But they are also more volatile and riskier than the likes of bonds, particularly in the short run.

5. Volatility and investment risk are not always the same thing

Volatility is prices moving up and down whereas risk is failing to meet your financial goals and the potential for loss.

For instance, stocks can be more volatile in the short term, although historically they have tended to deliver stronger, long-term growth outcomes than more defensive assets.[5] Meanwhile, cash is generally more stable in the near term, although inflation can reduce its purchasing power over time.

6. Rebalancing can benefit portfolios

A portfolio that starts with 70% stocks/30% bonds will likely drift over time because asset prices move differently. Rebalancing to a target asset allocation can help maintain a portfolio’s intended risk profile over time.[6]

7. Time horizon can influence asset allocation

Short-term market movements can be difficult to predict, while long-term returns have historically been less volatile. Some investors with longer time horizons choose to allocate more to growth assets, such as shares.

8. There is no “perfect portfolio” for everyone

Different portfolios may suit different investors depending on their objectives and tolerance for risk. And since risk tolerance varies from person to person, the portfolio that suits each individual will also differ.

9. Costs matter

Management fees, trading costs, and taxes all reduce returns, especially when compounded over years and decades.[7]

Summing these key principles up, the academic research suggests that:

- Higher risk potential generally involves accepting more risk

- Diversification helps manage that risk

- Markets are hard to beat

- Asset allocation can play an important role alongside investment selection

- Keep costs low

- Match your portfolio to your time horizon

Working out the right investment mix

How can you determine the right portfolio mix of assets for you? Investors should develop a coherent and well-defined personal strategy for the allocation of assets. That strategy will be driven by four factors:

Risk tolerance

This refers to how you handle the market's ups and downs. Investors with a higher tolerance for volatility may choose to allocate more to growth assets such as shares.

Goals

What are you investing for? Investors seeking long-term growth may choose to allocate more to growth assets. Income-focused investors may prefer investments such as dividend-paying shares or bonds.

Time horizon

As alluded to previously, a longer time horizon can allow an investor to potentially take on more risk, versus a shorter one, where more defensive assets may be preferred by some investors.

Taxes and liquidity

An investor’s personal tax situation can influence how they structure their portfolio. An investor’s liquidity needs or cash requirements can also play a part in their investment mix.

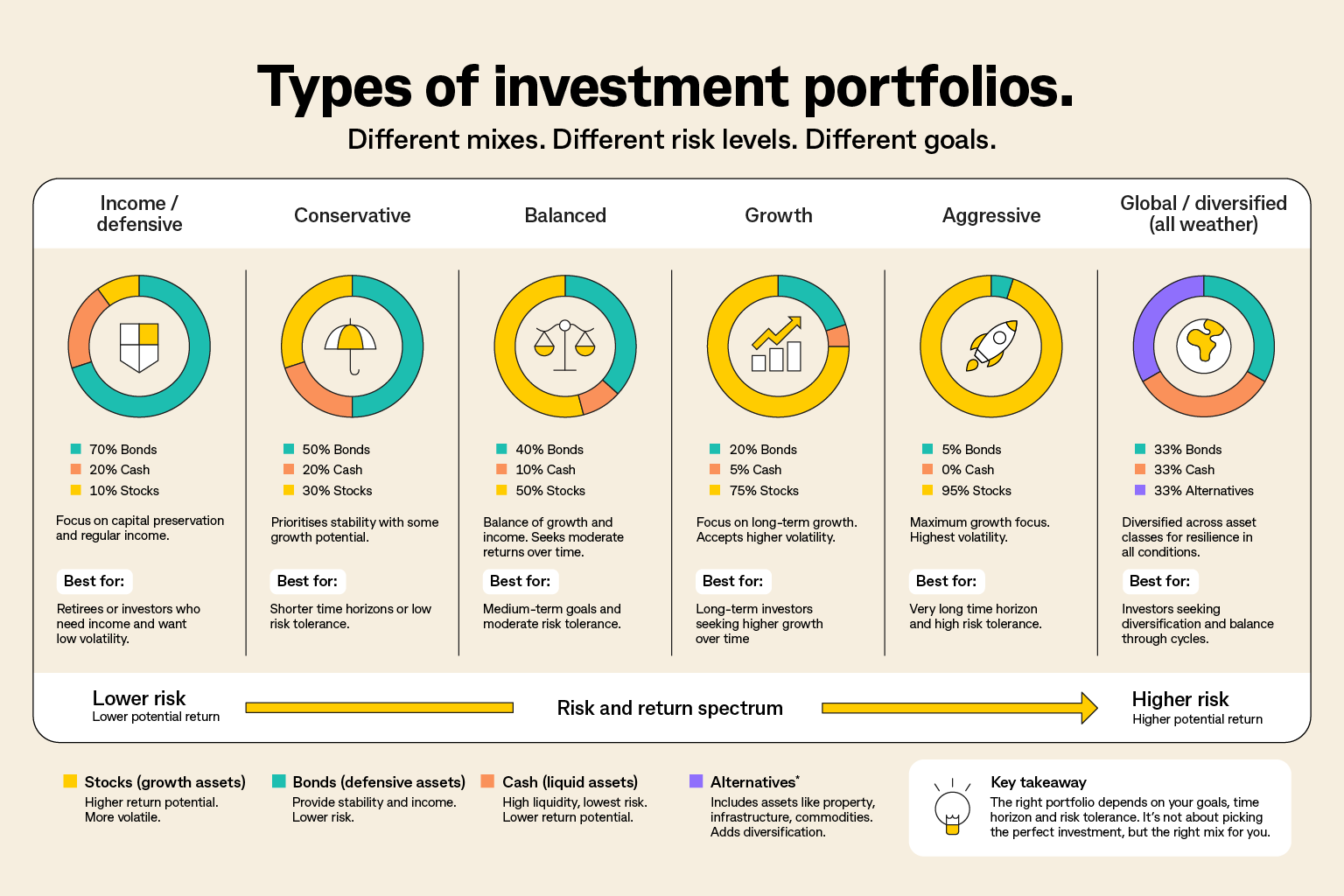

Types of investment portfolios

Based on the academic research, there are several simple investment portfolio types which have become industry standard:

1) Conservative portfolio

This type of portfolio is typically weighted towards bonds and cash, with smaller allocations to shares. The focus here is protecting money with low risk. Typical mix is 30% stocks/70% bonds and cash, or something similar.

2) Balanced portfolio

Typical mix is 50-70% stocks/30-50% bonds. This is a mix of growth and stability and is for people comfortable with moderate risk.

3) Growth portfolio

Typical mix is 70-80% stocks/20-30% bonds. It may suit investors with longer time horizons who are comfortable with higher levels of volatility.

4) Aggressive portfolio

Typical mix is +90% stocks/10% bonds. It may suit investors with a higher tolerance for risk and a long investment horizon.

5) Income portfolio

This is for those needing regular income, such as retirees. Typically, the portfolio includes dividend-paying stocks, bonds, and possibly REITs.

Source: CommSec

Simple portfolio example

Let us turn to a practical example of how to build a simple portfolio:

You have some experience as an investor, can stomach market downturns, and want to capture growth in the markets over time. You opt for a 70% equities/30% bonds portfolio.

The question is: which stocks and bonds should you invest in?

On stocks, is it best to go for 100% in Australian equities, or should you also mix in international shares? On this question, there is surprisingly little local research on the issue. US studies have suggested that putting 20-40% of your stock portfolio in global stocks helps reduce risk and lift returns.[8]

Yet Australia is different from the US as our stock market represents just 2% of global market indices. Does that mean that an investor should put only 2% of their stock portfolio in local shares? Most investors are comfortable holding more Australian shares, and there may be a tax benefit in having local stocks, through franked dividends.

Given this, many Australian investors choose to maintain a higher allocation to local shares.

For example, an investor could choose a 30:70 split between Australian and international shares.

On bonds, there is similar research on the benefits of international diversification for reducing risk and enhancing returns.[9] Because of this, an investor could choose a 30:70 split between Australian government bonds and international, currency-hedged government bonds.

The growth of exchange-traded funds (ETFs) has made diversified market exposure more accessible for many investors. It’s now possible for an investor to get broad market exposures via ETFs listed on the ASX.

Examples of widely used Australian share ETFs include VAS (Vanguard) and IOZ (iShares). VAS tracks stocks listed on the ASX 300, while IOZ covers the top 200 shares.

Examples of international share ETFs listed on the ASX include, VGS (Vanguard), IVV (iShares), and BGBL (Betashares). Note that IVV has pure US exposure while BGBL has global exposure.

With Australian government bonds, VGB (Vanguard), VAF (Vanguard), and IAF (iShares) are popular options. Note that VAF has broad Australian bond exposure, with government and corporate bonds, IAF has similar broad exposure, while VGB is pure government bonds.

For hedged international government bonds, VBND (Vanguard), VIF (Vanguard) and IHWL (iShares) are the largest ETFs.

Source: ETF providers, CommSec

Some investors may also consider diversified ETFs that provide exposure to multiple asset classes within a single investment. For example, Vanguard’s VDGR ETF offers a portfolio that invests in 70% growth assets (shares) and 30% defensive assets (e.g. bonds). Investors should consider fees, investment objectives and underlying asset allocations when comparing products, such as these.

Alternative portfolios

Portfolios do not have to be this simple. They can extend beyond stocks and bonds to include other asset classes such as cash, private assets, infrastructure, gold, and commodities.

Even within stocks and bonds, there is plenty of flexibility to tailor a portfolio to an individual investor’s needs. For example, the equity portion can be broken down into small caps, large caps, REITs, value, growth, dividend strategies, emerging markets, and more - the possibilities are almost endless.

That said, it is worth keeping in mind that added complexity can increase costs and may not necessarily improve investment outcomes.

We will take a further look at these alternative portfolios in a future article.

[1] Brinson, Hood & Beebower (1986), “Determinants of Portfolio Performance,” Financial Analysts Journal.

[2] Markowitz (1952) “Portfolio Selection,” Journal of Finance.

[3] See Markowitz (1952) “Portfolio Selection,” Journal of Finance.

[4] Markowitz (1952) “Portfolio Selection,” Journal of Finance, and Sharpe (1964) Capital Asset Prices: A Theory of Market Equilibrium under Conditions of Risk.

[5] Siegel (2014) Stocks for the Long Run (5th edition), and Dimson, Marsh, Staunton (2002) Triumph of the Optimists.

[6] Markowitz (1952) “Portfolio Selection,” Journal of Finance.

[7] See John Bogle, The Little Book of Common Sense Investing.

[8] On international diversification reducing portfolio risk, see Markowiz (1952), Portfolio Selection, Journal of Finance, and Solnik (1974), Why Not Diversify Internationally Instead of Domestically?, Financial Analysts Journal. For investors underinvesting abroad, see French and Poterba (1991), Investor Diversification and International Equity Markets, American Economic Review.

[9] See Solink (1974), Why Not Diversify Internationally Instead of Domestically, Financial Analysts Journal.