CommSec

CommSec

30 June 2026

Author: James Gruber is Equity Market Strategist at CommSec

Australian shares have stood the test of time. The ASX has been one of the best performing markets in the world over the past 125 years, up close to 10% per annum over that time.

It’s mirrored the rise of our country, aided by abundant resources, migration, and stable government and institutions.

Since the 1990s, we have had the privatisation of large firms, the entry of super funds which bought into the market, the extraordinary bull market in property, more companies heading overseas and some being success stories, more retail investors buying shares as investing was democratised, with the advent of exchanged-traded funds accelerating that trend.

The positive story has taken a hit of late, though. This year with the All Ordinaries up 0.2% to the end of May, it does not compare well, given the bull market happening overseas. The MSCI World Index is up 10%, the S&P 500 up 11% and the Nasdaq 20% higher.

Some of the discrepancy can be put down to (over?) enthusiasm for US technology stocks, but a look at Australia’s medium-to-long-term performance raises some interesting considerations.

Over the three years to the end of 2025, the ASX All Ordinaries Accumulation Index has risen 11.7% per annum, versus the MSCI World Index at 22.1% and the S&P 500 at 23.7%.

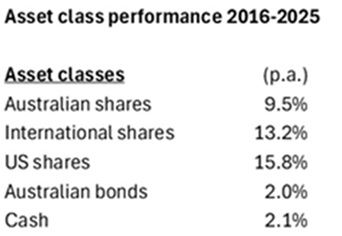

Over 10 years to the end of 2025, the ASX All Ordinaries Accumulation Index added 9.5% per annum, versus the MSCI World Index at 13.2% and the S&P 500 at 15.8%.

Note: Australian shares = All Ordinaries Accumulation Index, International shares = MSCI World ex-Australian Net Total Return Index, US shares = S&P 500 Total Return Index, Australian bonds = Bloomberg AusBond Composite 0+ Year Index, Cash = Bloomberg AusBond

Source: Bloomberg Finance L.P.

Over 20 years to the end of 2025, the ASX All Ordinaries Accumulation Index has climbed 9.7% per annum, versus the MSCI World Index at 10.3% and the S&P 500 at 12.1%.

What’s the story?

Why has Australia significantly underperformed other developed markets, especially the US, since this bull market began in 2009?

There are a lot of factors at play. We had a mining boom that petered out in 2011-2012 and since then, productivity growth has largely stalled. As a result, GDP growth has slowed materially.

The reasons for this are complex but much of the issue stems from Australia becoming a high-cost place to do business. Our companies have become less competitive, especially compared to overseas ones.

The slowing economy has resulted in wages flatlining in real terms (when taking inflation into account).

Managing cost of living pressures has become particularly hard for many households since inflation surged in 2022, pushing up day-to-day expenses.

That has weighed on domestically focused ASX-listed companies, which rely on consumer spending.

Given our slowing economy, some listed companies have aggressively expanded overseas over the past decade. Those expansions have not always been successful, with companies such as Reece and James Hardie recently experiencing share price pressures following offshore challenges.

Even long-standing international blue chips like CSL and Cochlear have also had major missteps which have cost their shareholders dearly.

It also has not helped that the ASX has relatively limited exposure to technology, with tech being just 3.7% of the ASX 200 index. That compares to the S&P 500, where technology is 38% of the index, and arguably greater than 50% when tech shares included under different sectors - such as Alphabet, Tesla, Amazon and Meta – are accounted for.

The latest concerns are around Federal Budget measures that affect the future tax treatment of investment assets, including shares, which have added to investor uncertainty around the outlook for Australian equities.

Given the recent underperformance of Australian stocks, many are asking whether the local market is still worth investing in.

It’s clear that more money is heading overseas right now. Data from the ASX shows that ETFs, and international equities are getting huge inflows compared to Australian shares and other asset classes.

In the first quarter of this year, international equity ETFs received $6.9bn in flows, compared to Australian equity ETFs of $4.1bn, and Australian fixed income at $2.1bn.

In 2025, it was a similar story. International equity ETFs received $19.9bn in flows, versus Australian equities with $13.3bn and Australian fixed income with $8.4bn.[1]

Seemingly, investors are voting with their feet.

But the Australian share market should not be written off so easily. After all, commodities are a large slice of the ASX 200, and they have long been a tale of boom and bust. A reasonable argument could be made that Australia’s commodity sector may benefit from the enormous resource requirements associated with the buildout of artificial intelligence infrastructure.

Though it’s easy to extrapolate from our flatlining economy at present, it will not stay like that forever, and the economy will turn around at some stage, to the benefit of domestic-facing companies.

We may also benefit from the deployment of AI through lower business costs and improved productivity over time.

On a relative basis, our market looks less expensive than many others. On almost every major valuation metric, the US is very expensive versus its history. At current price-to-earnings ratio levels, the 10-yr annualised return of the S&P 500 has historically been subdued, falling within a range of +2% and –2%.

In sum, the Australian market may be down, but it is not out.

[1] ASX investment products monthly reports