CommSec

CommSec

31 Mar 2026

Author: James Gruber is Equity Market Strategist at CommSec

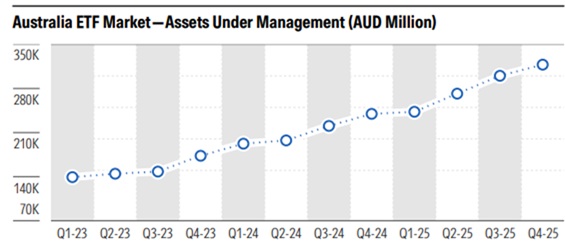

Australian investors love ETFs (exchange-traded funds) - for their convenience, simplicity, and liquidity. In 2025, the ETF industry grew 34% year-on-year to $330 billion. Over the past decade, ETF assets under management have risen more than 16x.

Source: Morningstar

ETF Basics:

What is an ETF?

An Exchange-Traded Fund or ETF is a type of investment fund traded on stock exchanges. It pools money to invest in a diversified basket of assets - such as stocks, bonds, or commodities - often designed to track a specific index, offering low-cost exposure to various markets through one trade.

The different types of ETFs

You can get different ETFs by asset class (stocks, bonds, cash, and so on), geography (Australia, international, emerging markets and others), style (active versus passive), and strategy/special features (leveraged, dividend, inverse).

Risks to investing in ETFs

ETFs are not risk-free. Here are some of the investing risks:

A broad market ETF (like the ASX 200) will not protect you in a market crash.

If you invest overseas, currency movements can affect returns. When the Australian dollar strengthens, your international ETF returns shrink, and if the Australian dollar weakens, your returns improve.

Market-cap weighted ETFs can be heavily dominated by a few companies, and sector ETFs (e.g. tech) may be even more concentrated.

Some ETFs are thinly traded and can be hard to exit during times of market stress.

Thematic ETFs can list when there is hype around them and therefore be more volatile.

Some ETFs are higher risk, such as leveraged ETFs which magnify gains and losses.

Bond ETFs fall when interest rates rise.

ETFs do not always perfectly track indexes due to costs, rebalancing etc.

International ETFs can involve foreign tax withholding.

Many investors opt for ETFs that capture a whole market, such as the Australian or US stock market. There is nothing wrong with this, though it is important to understand that these types of ETFs typically track indices, such as the ASX 300 or S&P 500, and these indices can have certain quirks or tendencies.

For instance, the ASX 300 has a heavy emphasis on financials and resources. Together, these make up 61% of the index, which is reflected in ETFs that track it. The likes of technology (2.5%) consumer staples (3.4%) and energy (4%) have little weight in the index.

Some investors may want more exposure to higher growth sectors such as technology. The ASX 300 index and ETFs are not going to give them that.

On the flip side, the S&P 500 leans heavily on technology stocks. If you add the likes of Amazon and Tesla – classified as consumer discretionary stocks in the S&P – and Meta and Alphabet – included in the communications sector – to the technology sector, then tech accounts for more than 40% of the S&P 500 index.

Be aware that having +40% exposure to one sector can bring elevated risk should that sector falter.

The bottom line is that indices and the ETFs that track them can be skewed in a certain way and it is important for investors to be across the nuances so that they can match the funds with their own needs and risk requirements.

2. Thematic ETFs have stock/sector risks

Thematic ETFs have become popular over the past year. Now, you can get ETFs in big themes such as global defence to more niche ones such as video games and electric vehicles.

One risk to highlight with these thematic ETFs is that unlike with whole market ETFs, you have greater exposure to certain sectors and stocks. That can be a positive if they go up in price, but a negative if they all move down at once. Concentrated bets on themes can bring heightened risks if not managed carefully.

3. International ETFs can have currency effects

ETFs with overseas exposure can have currency risks if they are unhedged. Hedged ETFs reduce the impact of currency movements on investments. Unhedged ETFs do not, leaving investors exposed to currency movements.

For example, you may invest in an ETF that tracks the S&P 500 index. If it is unhedged and if the Australian dollar strengthens after you buy it, your returns in AUD may drop, even if the underlying investments do well in their home currency. Conversely, if the Australian dollar declines, the value of an unhedged ETF may rise in AUD terms, assuming the underlying asset holds or increases in value.

Hedged ETFs typically come at a higher cost to unhedged ETFs.

4. Leveraged funds amplify returns

There are now many geared ETFs on the markets. These ETFs use debt to amplify returns.

For instance, some target 2x the daily return of the ASX 200. In theory, if the ASX 200 goes up 1% in a day, these ETFs would increase 2%. Conversely, if the index drops 1%, the ETFs would fall 2%.

Geared ETFs are generally more volatile than the average ETF and are therefore more suited to experienced investors.

5. Active versus passive ETFs

There are more active funds listing as ETFs on the ASX. Unlike passive ETFs, these funds do not passively track an index or indices. They actively manage their holdings with the aim of outperforming a benchmark.

With active funds, you are relying on the skills of the managers and the investments that they make.

Typically, active ETFs have higher costs versus passive funds.

6. Costs vary for ETFs

Costs for ETFs can differ quite a bit. The cheapest ETF in Australia has a management expense ratio is just 0.03%. Meanwhile, higher cost ETFs can run at greater than 1%.

Typically, passive ETFs that track indices carry lower fees than active ETFs managed by fund managers. Also, thematic ETFs are normally higher cost than those that replicate an index.

Costs matter, especially over the long term, and it’s one of the many factors that are taken into consideration when developing financial plans.