CommSec

CommSec

15 May 2026

Author: James Gruber is Equity Market Strategist at CommSec

Equity funds and fund managers spend almost every waking hour analysing markets. They often have decades of market experience and knowledge. They have access to the best data. They meet companies and CEOs on a regular basis.

How can individual investors possibly compete against them?

Having been a fund manager and an individual investor, your author believes the latter has some significant advantages that are not highlighted enough:

1. Size

“A fat wallet is the enemy of superior investment results.”

-Warren Buffett

“Size, at a certain point, gets to be an anchor, which drags you down. We always knew that it would.”

- Charlie Munger, Buffett’s former offsider

Did you know that the world’s greatest investor Warren Buffett’s investment performance has trailed off since the 1980s? Or, that his best individual year was in 1976, 50 years ago?

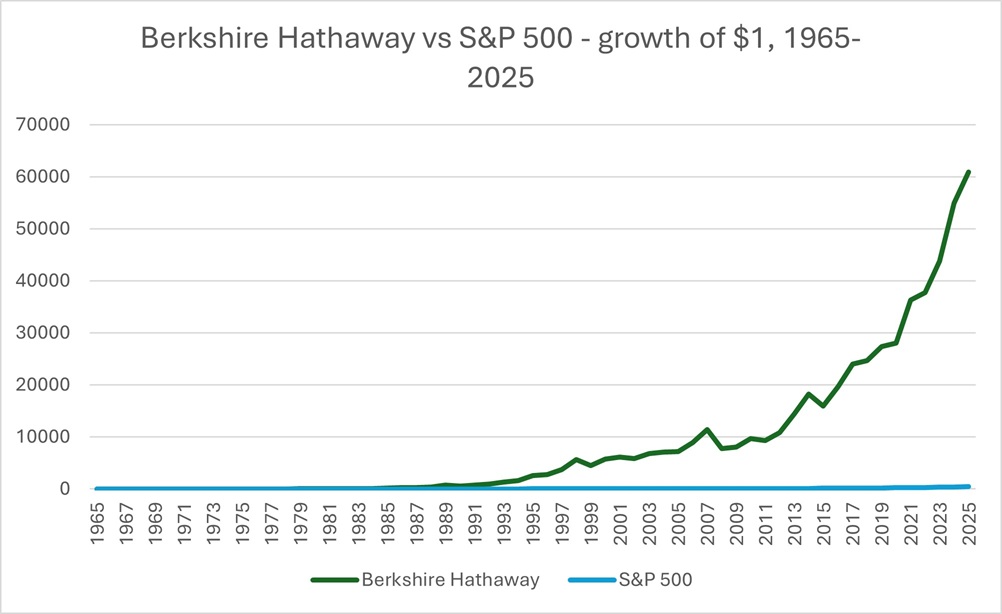

That may not be apparent in this first chart:

Source: Berkshire Hathaway, CommSec

Because of this, the individual investor can have a distinct advantage over the fund manager who has billions to invest.

2. Time

There are large fund managers out there that promote themselves as being ‘long-term investors’, but there is often a heavy focus on the performance of funds in the short-term.

There is a saying in the investment industry that investors can excuse one year of underperformance for a fund, and even two years, but a third year won’t end well.

This pressure to achieve short-term results can harm investment performance. It can lead to over-trading and higher costs. It can lead to emotive decision making. It can mean overreacting to short-term events.

If fund managers do not play the short-term game, they can put their careers at risk.

Individual investors do not have to play the same game. They can play the long game, invest patiently and prudently, and not have to change course at a moment’s notice.

3. Investing in what you know

Peter Lynch is known as one of the most successful-ever fund managers. Managing the Fidelity Magellan Fund, he achieved 29.3% average annual returns from 1977-1990.

Yet, in his book ‘One Up on Wall Street,’ Lynch suggests that individual investors can have an advantage over professional investors: everyday consumers can spot winning companies before analysts or fund managers do. He argues that individuals encounter products, services, and trends in daily life - giving them early insight into potential investment opportunities.

For instance, many small business owners had used accounting software, Xero, over the past 15 years, giving them unique insights into the product and company – insights that could have led them to invest in the company. Xero listed on the New Zealand Stock Exchange with a market capitalisation of just A$51m in 2007 and was worth $450m when it dual listed on the ASX in 2012. Today, its market capitalisation is $13.3bn, having reached a peak value of $33bn mid last year.

Or if you have a daughter, you might have been aware very early on that Lovisa was attracting teenagers with its cheap and cheerful jewellery, well before it became a stock market darling. Lovisa listed with a market capitalisation of $210m in 2012 and today is valued at $2.3bn.

It shows that $1 invested in Buffett’s Berkshire Hathway in 1965 has turned into almost US$61,000, a return of more than 6,000,000%, or 19.8% per annum (p.a.) That compares to $1 invested in the S&P 500 over the same period turning into US$455, or a cumulative return of 45,362%, or 10.6% p.a.

It means Buffett has beaten the index by more than 9% p.a. over 60 years - an amazing feat.

But it does not tell the full story.

When Buffett took over Berkshire in 1965, he had a relatively small amount of money to invest. Because of this, he was able to be nimble, invest in micro stocks, and force changes at businesses he invested in, if necessary.

These advantages allowed him to achieve extraordinary returns in the initial years. Throughout the 1960s, he outperformed the S&P 500 by a stunning 27% p.a. In 1965 alone, he beat the market by 37%.

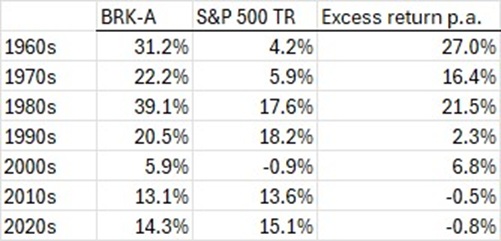

Berkshire Hathaway since May 1965

Source: Owen Analytics, Firstlinks, CommSec

His best individual years all featured before 1990. In 1976, he beat the market by 105%, and in 1979, he crushed the index by 84%.

Yet, from around 1990, something changed. Buffett still had good performance, beating the index in the 1990s and 2000s, but it was not the same as before. Since 2010, he has underperformed the S&P 500.

What’s happened is not so much that Buffett’s abilities have declined. Instead, it has been more that the success of Berkshire Hathaway has produced so much money that Buffett has struggled to get the returns he once did.

For instance, Berkshire now holds US$382 billion in cash, which is more than the market capitalisation of 480 of the companies in the S&P 500 Buffett has repeatedly said that it’s difficult for him to put this amount of money to work and achieve adequate returns for Berkshire’s shareholders.

The moral of the story? Size can be the enemy of the investor.

Individual investors can get these types of insights before fund managers and use them to their advantage, Lynch says.

4. Flexibility

To appeal to investors, funds may label themselves – as value, growth, compounders, or Buffett-like – to give a guide as to how they invest. This makes sense, though it can constrain them.

If a value fund invests in a high-growth, high priced growth stock, it could lead to concerns about “style drift” and even downgrades from the consultants and firms who rate these funds.

Individual investors do not have the same constraints. They can go where there are the most opportunities, whether they be value, growth or something else.

That could help performance over the long-term.