CommSec

CommSec

5 May 2026

Author: James Gruber is Equity Market Strategist at CommSec

In recent years, defence has been one of the market’s trendiest sectors, both locally and overseas. Strong structural drivers have contributed to its rise.

The Russia-Ukraine war beginning in early 2022 kickstarted it.

Before this, European countries thought it unlikely that there could be a war on the continent. Consequently, defence spending in Europe was low and militaries were generally under-resourced.

Russia’s invasion changed that. War in Europe became a real and immediate threat, and governments began to view defence as essential rather than optional.

Soon after, Germany announced a historic €100bn special defence fund. This was significant as Germany had been reluctant to use military power before that.

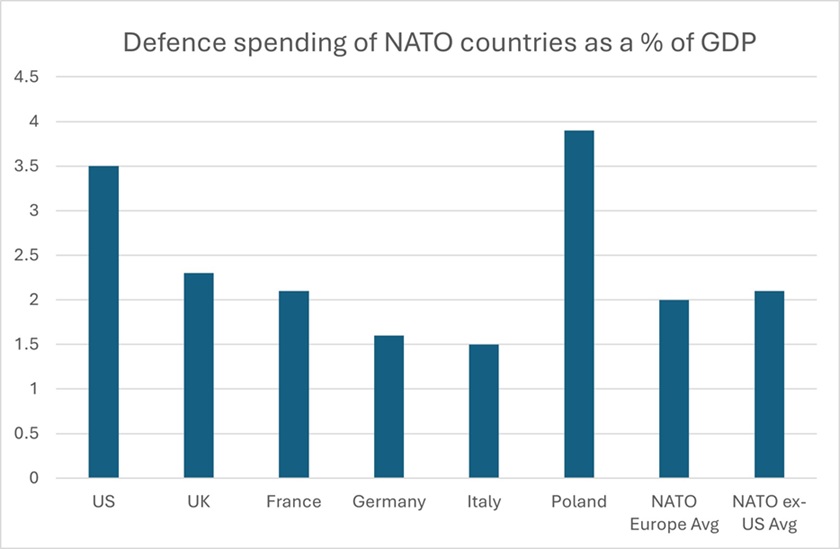

NATO members also accelerated moves to reach the organisation’s 2% target for defence spending as a percentage of GDP.

In early 2025, Donald Trump was elected to a second term as US President and his core message to Europe – dating back to his first term – was that it was not paying its fair share for defence. He repeatedly criticised NATO for not meeting its 2% of GDP defence target and pushed for much higher targets of up to 5%.

NATO has since agreed to the 5% of GDP target by 2035. It committed to 3.5% of GDP for core defence such as troops and weapons, and 1.5% of GDP being spent on broader security such as cyber security and infrastructure.

Currently, NATO members spend about €1.4tn on defence. At 5% of GDP, it would require increased spending of more than €1tn a year, or an increase of more than 70%.

Source: NATO, CommSec

It is not just Europe, though. Trump’s message that all countries need to spend more on defence has resonated, with global defence spending having increased by almost 30% over the past three years – the fastest defence spending expansion since the 1980s.

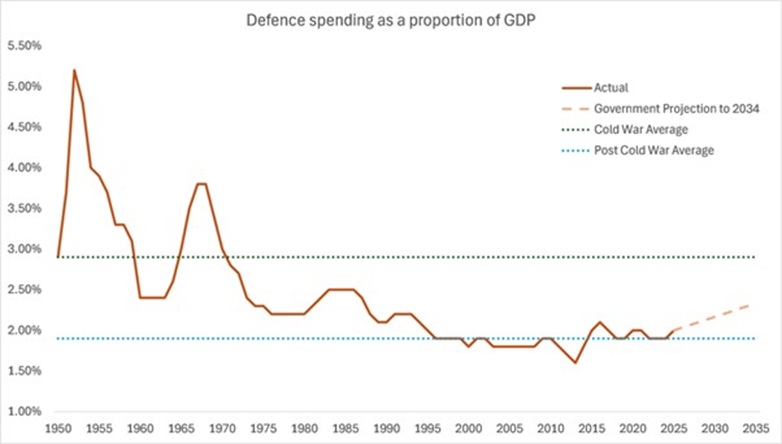

Australia has committed to spending more too, albeit in a smaller way. Currently, we spend around 2% of GDP on defence. Under government projections, that will increase to 2.3% by 2033-34.

Source: SIPRI Military Expenditure Index and Australian government projections

The recent Iran War has also brought defence capabilities into sharper focus.

The theme has not been lost on investors

Given these tailwinds, investors have jumped on the defence theme. European defence stocks were the first to take flight. Since the start of 2022, shares in Germany’s Rheinmetall – specialising in land systems and munitions – have risen 16x, Leonardo’s – an Italian aerospace and defence group - has increased 8x, while defence contractor BAE Systems has gained 3x.

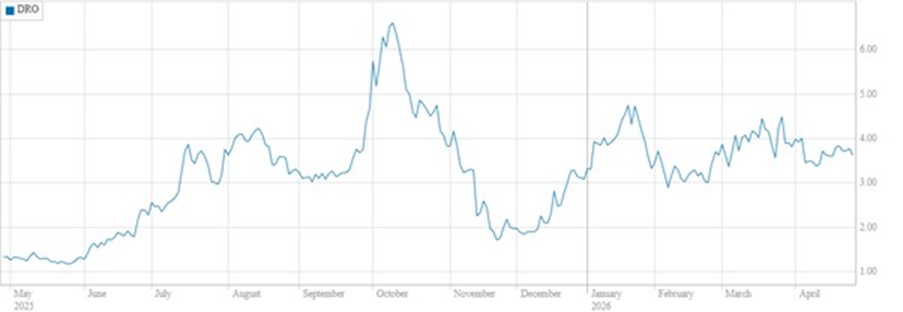

The trend has also played out in Australia. Over the same period, shares in DroneShield – a counter-drone technology firm – have risen 21x, those of Electro Optic Systems – a defence contractor - are up 2.7x, and shares in Austal – a navy ship builder – have gained 1.5x.

DroneShield share price

Source: CommSec

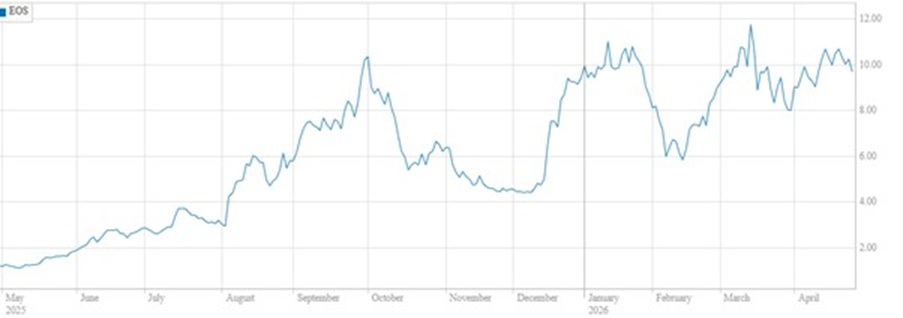

Electro Optic Systems share price

Source: CommSec

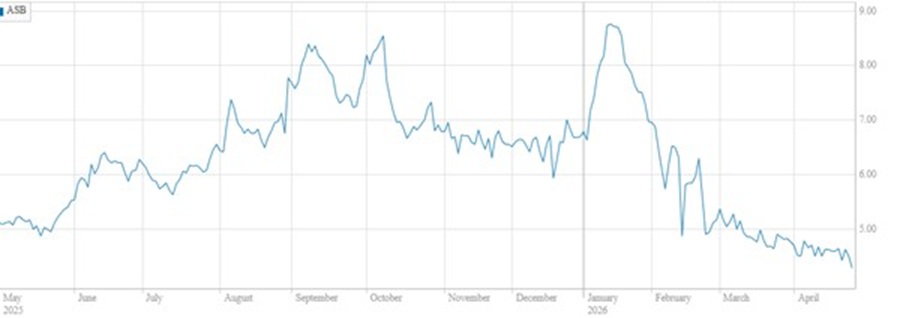

Austal share price

Source: CommSec

Drilling down on the Australian defence companies

Here is a brief overview of the businesses of Australia’s largest defence stocks on the ASX:

DroneShield (ASX: DRO)

Drones have quickly grown into a key weapon in modern warfare. Increasingly, they are used for precision strikes with explosives.

DroneShield has developed a niche in counter-drone technology. It offers a range of equipment for detection and neutralisation, including vehicle-based, handheld, and fixed-site products. It aims to be a one-stop shop.

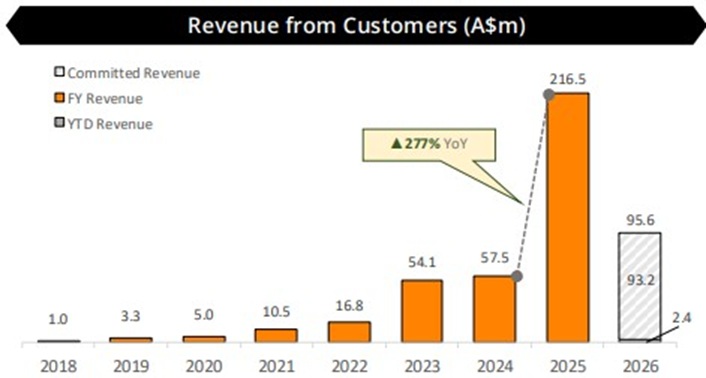

It was one of the earliest companies in counter-drone technology and that first-mover advantage has helped it grow revenue from $5m in 2020 to $227m in 2025.

Source: SIPRI Military Expenditure Index and Australian government projections

Most of the revenue comes from military forces in the US. It predominantly sells hardware, but a growing number is from software as a service as the company’s AI software requires continuous updates. DroneShield introduced a subscription service in 2021 to take advantage of this.

The company has spent up to 20% of revenue on research and that has depressed profits. What net margins it may achieve in future is a key question.

Risks primarily revolve around competition, with big players in the market, including Leonardo from the UK.

Besides competition, the other main risk is obsolescence, with the possibility of superior technology emerging.

Recently, the Chairman and CEO decided to step down from their leadership positions , resulting in a sharp, one-day drop in the share price.

Electro Optic Systems (ASX: EOS)

This company is one of Australia’s oldest defence contractors. It designs and manufactures remotely operated weapons systems, vehicle turrets, and technology for detecting and shooting down military drones.

It specialises in lethal weapons, including the R150 and R800 remote weapons platforms, which are mounted on naval vessels and military vehicles, allowing operators to engage targets from a safe distance. Their ability to be remote controlled makes them a valuable tool in warfare, for both offensive and defensive purposes.

The company has a strong order book of $459m, up from $136m at the end of 2024. It aims to realise 40-50% of this order book in 2026.

The company is a small defence contractor on the global stage and that may be why it has continued to struggle to post underlying profits in recent years (FY25 underlying earnings were -$24m).

Nonetheless, it could benefit from the increased global spending on defence going forward.

In March, its the shares had a big drop after it was revealed that the CEO and CFO intended to sell a large portion of their stakes in the company.

Austal (ASX: ASB)

Austal builds and maintains military ships, mainly for the US Navy. It designs and constructs vessels like fast transport ships, patrol boats, and support and logistics ships. It also repairs and upgrades ships as well as provides ongoing maintenance services.

Austal has a track record as a shipbuilder for defence forces, and it could benefit from the expected ramp up in global defence spending.

One risk is that it is the only foreign-owned contractor that builds and maintains warships for the US. If America decides that outsourcing this function to foreigners does not make sense, then Austal may be impacted.

Considerations for investors

Global defence spending looks set to soar over the next decade. That is well known in markets, and the question for investors is: how much of it is in company share prices?

That depends a lot on how much the ASX-listed businesses can continue to take market share and grow their order books in coming years, and that will depend on creating and maintaining superior technological products versus their peers.