CommSec

CommSec

4 May 2026

Author: James Gruber is Equity Market Strategist at CommSec

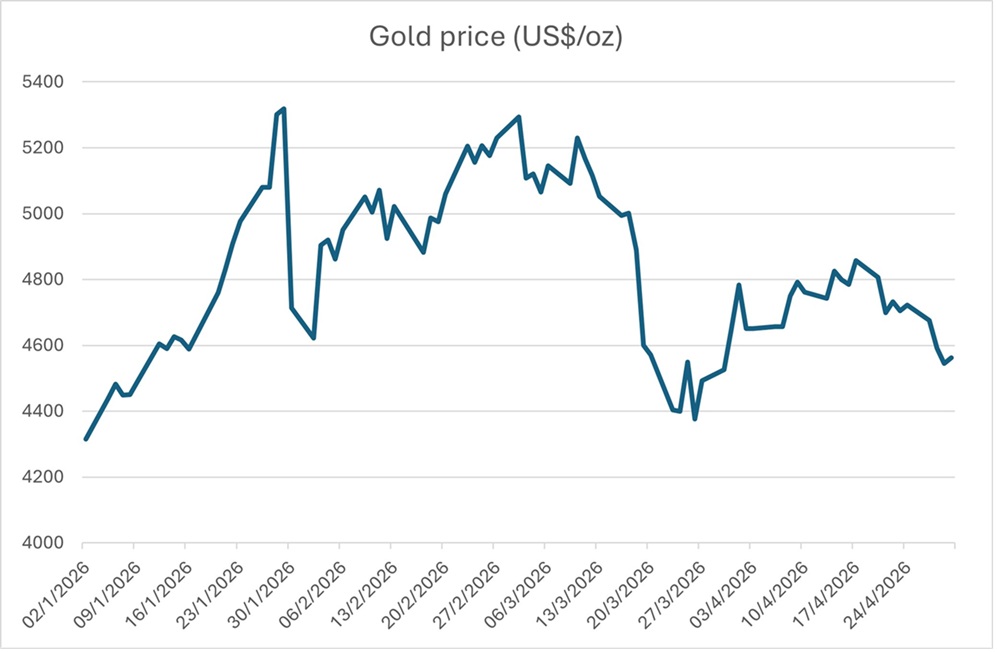

One curiosity during the US-Iran War is the price action of gold. Traditionally, it has been seen as a beneficiary of war and pending inflation, but not this time. The question is: why?

Source: LSEG, CommSec

What propelled gold higher before the war

To answer this question, we need to go back to what drove gold higher in the first place.

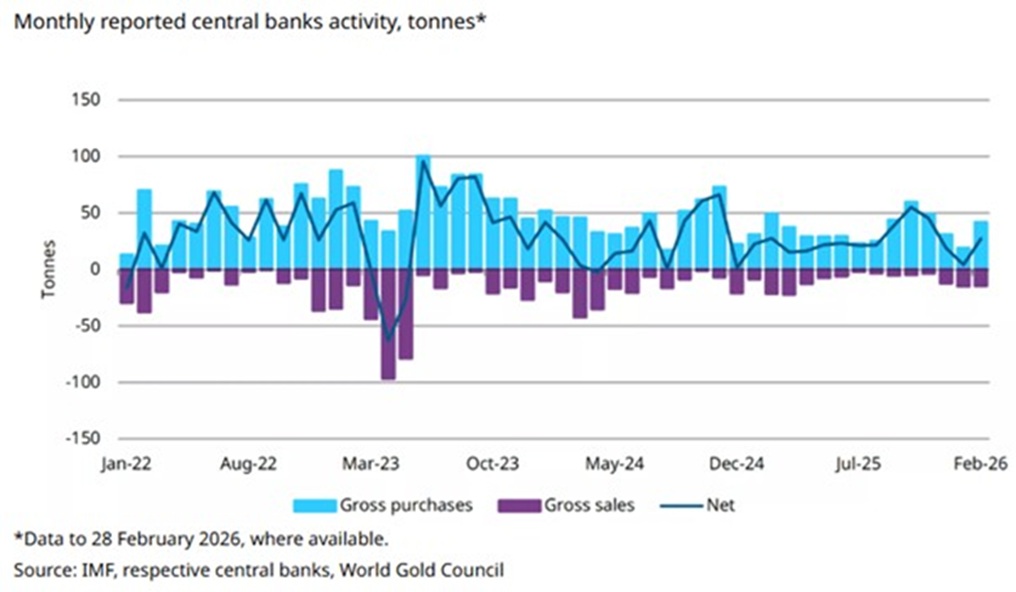

The gold bull market really gathered steam from 2022, and that is not a coincidence. It was at the start of that year that Russia invaded Ukraine. The US and its allies then froze about US$300 billion of Russia’s foreign exchange reserves. This hamstrung Russia’s central bank, but it also sent a signal to other countries that their reserves could be frozen at any time. In other words, their holdings in the likes of US Treasuries were not as safe as previously assumed.

That spurred many central banks to buy large amounts of gold, which was deemed by them to be a safe alternative to holding US-denominated assets.

These central banks bought gold en mass and have largely been big net buyers ever since. That boosted overall demand for gold.

These central banks sold US assets such as the US dollar and Treasuries to buy gold. That may be partly why the US dollar index – the dollar measured against a basket of other currencies – peaked in October 2022. It’s also worth noting that 2022 marked a period when central banks aggressively raised interest rates to rein in the hottest inflation in decades after the pandemic.

The other factor that drove gold to record prices was increased buying from retail investors. You might recall the large lines outside of gold bullion stores in Australia, especially in September and October last year.

That propelled gold prices to reach an intraday record of US$5,589 an ounce in late January.

Since then, and especially after the war began, prices have fallen sharply, albeit there has been a small recovery recently.

So, what changed?

What has led to the fall in gold prices?

Though official figures are not in, it is likely that the speculative frenzy that pushed gold prices higher in 2025 has dissipated as prices have fallen. The high prices may have also led to central banks potentially taking profit on large gains from the metal.

Related to this has been a strengthening US dollar since the Iran war started. Gold is globally quoted in US dollars so when the dollar strengthens, gold becomes more expensive in other currencies, which can result in demand softening, and prices to fall.

This hints at another potential reason for gold’s recent plunge. That is, rising real yields. When real yields (bond yields minus inflation) rise, it makes no yielding assets like gold less attractive.

What may happen next

Stepping back from the noise of the war, gold’s fate is likely to be intertwined with the fate of the US dollar. In this context, it can be helpful to view gold as an alternative currency. After all, prior to 1971, gold reserves were the backbone of the global monetary system, before the US dollar took on that role.

In recent years, doubts about the future of the US dollar have arisen with the US running a trade deficit of 6% of GDP and having government debt to GDP of close to 100%, near the highs reached during World War Two. The current US President, Donald Trump, has further increased the deficit through a combination of tax cuts and higher spending.

Over time, the US dollar is likely to suffer if America continues to run high and increasing deficits, and if that happens, gold could prove to be an attractive alternative.